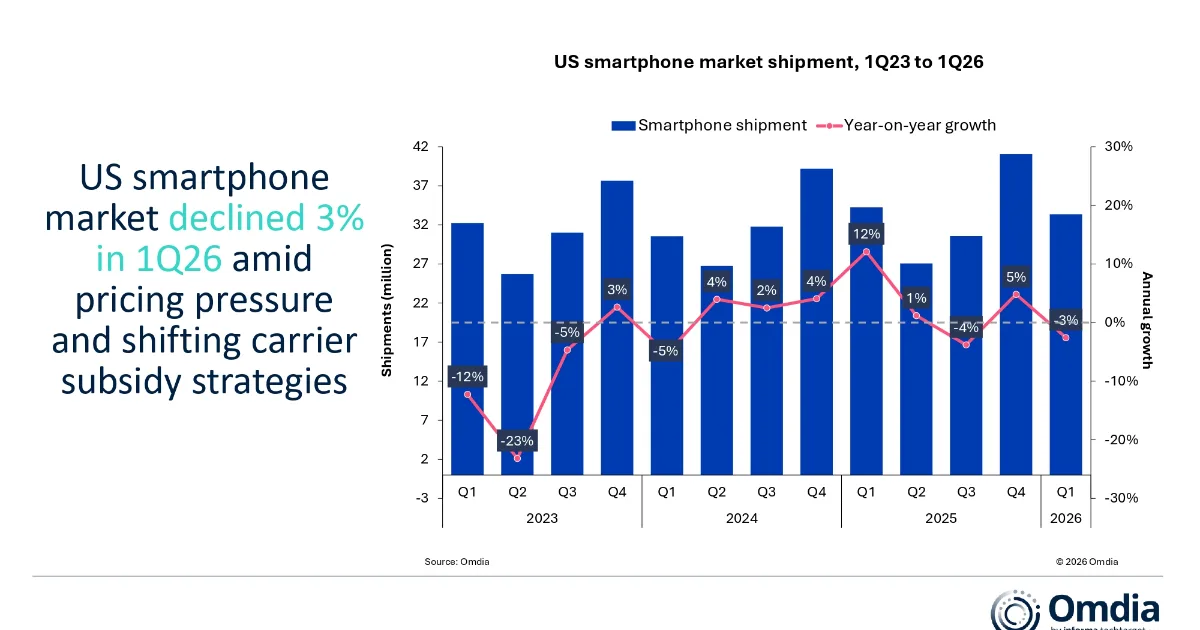

The U.S. smartphone market declined 3% year over year in the first quarter of 2026, according to the latest research from Omdia. Smartphone shipments in the country reached 33.4 million units during the quarter. On the surface, the drop appears moderate. But beneath the headline figure, the market is showing clear signs of structural change.

Premium devices and ultra-low-cost models remained relatively resilient. By contrast, smartphones priced between $300 and $799 came under significant pressure. The decline was especially visible in the mid-priced Android segment, where consumers are facing higher costs, weaker subsidies and less compelling product differentiation.

Part of the decline reflects a base effect. In the first quarter of 2025, suppliers and mobile carriers had built up inventory in advance of possible U.S. tariff measures. That created a higher comparison point for 2026. But the latest contraction cannot be explained by the base effect alone. Omdia said restrained carrier upgrade activity, rising memory and storage costs, and delays in major premium model launches all weighed on shipments.

The report’s core message is that the U.S. smartphone market is no longer moving as one. The premium market, led by high-end iPhones, is being protected by carrier financing and promotions. The sub-$300 segment is benefiting from prepaid demand and pre-orders ahead of price increases. But the middle of the market is being squeezed from both sides.

Apple Held Its Ground, While Samsung Was Hit by Launch Delays

Apple maintained its lead in the U.S. smartphone market in the first quarter of 2026. Its shipments declined 3% year over year, but the delayed launch of Samsung’s Galaxy S26 reduced direct competition from premium Android devices, helping Apple defend its position.

According to Omdia, the iPhone 17 series accounted for 70% of Apple’s shipments, while prepaid promotions for the iPhone 15 supported demand at the lower end of the market.

Apple’s strength in the U.S. is not based only on product competitiveness. The iPhone is deeply tied to carrier installment plans, trade-in programs and plan-based promotions. Even when retail prices rise, many consumers experience the cost through monthly payments rather than the full device price. That structure gives premium devices greater resilience.

Samsung ranked second, with shipments down 5% year over year. The main factor was the delayed launch of the Galaxy S26. Still, demand for the model itself appeared strong, with pre-orders for the S26 series rising about 25% compared with the S25 series. During the quarter, Samsung relied heavily on demand for its A-series devices in prepaid channels, particularly the Galaxy A17.

This points to a dual challenge for Samsung in the U.S. market. At the premium end, it must compete directly with Apple. At the entry level, it faces brands such as Motorola that offer strong price competitiveness. As the mid-range and upper-mid-range Android segments weaken, Samsung must refine the value positioning between its A-series and S-series devices.

Motorola Emerges as the Hidden Winner of the Low-Cost Market

Motorola was the standout performer in the quarter. Omdia said Motorola was the only major vendor to grow, with shipments rising 18% year over year. The key driver was its refreshed Moto G portfolio, which accounted for more than 70% of Motorola’s quarterly shipments.

Motorola’s growth reveals another side of the U.S. market. While premium demand remains concentrated around Apple, prepaid and low-cost channels are becoming more price sensitive. Under pressure from inflation and wireless service costs, some consumers are choosing practical, affordable devices over the latest flagship models.

Inventory dynamics also helped Motorola. Carriers and prepaid channels moved to secure stock ahead of Motorola’s April price increase, supporting first-quarter shipments.

Motorola’s performance shows that the smartphone market is not simply stagnating because of a lack of innovation. The market is still moving, but growth is splitting between expensive premium devices and highly affordable practical models. The middle is becoming harder to defend.

Google Pixel Faces Limits in Premium Expansion

Google’s smartphone shipments fell 7% year over year in the first quarter of 2026. Omdia said the Pixel 10 series failed to repeat the momentum that the Pixel 9 series had generated a year earlier. The early launch of the Pixel 10a helped offset part of the decline, but Google still depends heavily on aggressive carrier promotions to expand Pixel demand.

Google’s challenge is the gap between technical reputation and sales scale. Pixel devices are known for AI features, camera software and a clean Android experience. But in the U.S., Google does not have the same breadth of distribution, subsidy support or brand loyalty as Apple and Samsung.

This matters in a market where premium smartphone purchases are deeply connected to carrier promotions. Product differentiation alone is not enough to significantly expand share.

AI features are increasingly positioned as Pixel’s main selling point. But it remains unclear whether they are strong enough to persuade consumers to upgrade. That question will also shape the next phase of competition around AI-native devices.

The Market Is Polarizing by Price

Omdia’s data suggests that the U.S. smartphone market is becoming increasingly polarized. The premium segment above $800 declined only 1% year over year. The sub-$300 segment grew 8%. But the $300 to $599 segment fell 19%, while the $600 to $799 segment declined 6%.

These figures reveal a clear shift in consumer behavior. When consumers buy expensive phones, they often use carrier financing and trade-in offers to reduce the monthly burden. When consumers are highly price sensitive, they move toward prepaid plans and low-cost devices.

Mid-range devices are caught in between. They are not cheap enough to satisfy budget-conscious consumers, but they often lack the premium benefits, subsidies and ecosystem pull of flagship devices. Rising component costs also put pressure on manufacturer margins.

Mid-range Android devices are being hit hardest. Apple can defend multiple price points through its premium ecosystem and promotions on older iPhones. Android manufacturers, however, face price increases, intense competition and weaker subsidies at the same time. This makes the mid-range Android segment one of the most vulnerable parts of the U.S. smartphone market.

Carrier Subsidies Have Become the Market’s Shock Absorber

Another key theme in the report is the role of mobile carriers. Omdia said the U.S. smartphone market has entered a phase in which carriers are absorbing much of the consumer impact from rising device prices.

Suggested retail prices began rising in the first quarter of 2026. But carriers have softened the impact through installment financing, promotions and plan-based benefits. As a result, many consumers have not yet fully felt the effect of higher device costs.

This reflects a structural feature of the U.S. smartphone market. Many consumers do not buy phones outright. Instead, they purchase devices through long-term carrier installment plans. Monthly payments, trade-in values and plan benefits often matter more than the full retail price.

The question is how long carriers can continue absorbing this burden. If memory and storage costs continue to rise, tariff uncertainty persists and premium device prices keep increasing, carriers may reduce subsidies or attach them to more expensive service plans. That could further slow upgrade demand.

This is why Omdia identifies carriers’ ability to absorb pricing pressure as one of the most important variables for the rest of 2026.

Rising Component Costs and Launch Delays Could Extend Replacement Cycles

The pressure on the smartphone market is not only a demand-side issue. Costs are rising on the supply side as well. Higher memory and storage prices are worsening manufacturers’ cost structures. This can lead either to higher retail prices or narrower margins.

If manufacturers raise prices, consumers may delay upgrades. If carriers increase subsidies to offset those prices, carrier profitability may come under pressure.

Launch timing also affected the quarter. When major premium models such as Samsung’s Galaxy S26 are delayed, sales can shift across quarters, increasing shipment volatility. That makes inventory planning and channel order timing more important.

The U.S. smartphone market is becoming a more delicate game of inventory, pricing and promotions. New product launches no longer automatically generate replacement demand. Consumers are keeping devices longer, carriers are becoming more selective with subsidies, and manufacturers must manage product portfolios and launch timing more precisely.

2026 Outlook: Omdia Expects a 4% Annual Decline

Omdia expects these pressures to continue through the rest of 2026. Full-year U.S. smartphone shipments are projected to fall 4% year over year. In the near term, pricing, subsidies and inventory adjustments are likely to shape the market.

Over the longer term, AI-native devices are emerging as a new point of interest. Omdia does not expect such devices to replace smartphones in the immediate future. However, AI-based interfaces could gradually change how consumers perceive the value of upgrading a smartphone. Developments around OpenAI and Amazon’s interest in AI hardware are also seen as signals of this broader shift.

This raises a new question for smartphone makers: can AI features truly create replacement demand?

On-device AI, voice and visual interfaces, personal assistant agents and app-replacing AI experiences may eventually become important reasons to upgrade. For now, however, the answer remains uncertain. As the smartphone market matures, the next major upgrade cycle may need a stronger justification than a better camera or brighter display. Increasingly, that justification may have to come from AI experiences.

Conclusion: The Real Crisis Is Not the Decline, but the Collapse of the Middle

The 3% decline in the U.S. smartphone market in the first quarter of 2026 looks like a modest adjustment at first glance. But inside the market, a more important shift is underway.

Premium devices are holding up through carrier financing and Apple’s ecosystem strength. Ultra-low-cost devices are benefiting from prepaid demand and price-sensitive consumers. Mid-priced devices, however, are being hit hardest by rising costs, weaker subsidies and weaker differentiation.

This shift changes how smartphone makers must compete. It is no longer enough to release a good device. Companies must align price-tier strategy, carrier promotions, prepaid channel positioning, practical AI value and launch timing.

Carriers have become the shock absorber for consumer price increases, but they cannot carry that burden indefinitely.

The key question for the U.S. smartphone market in 2026 is not simply how much shipments will decline. It is why consumers should buy a new smartphone at all — and who will absorb the cost of convincing them.

Manufacturers and price segments that cannot answer that question may disappear from the middle of the market.