Corporate America’s AI adoption race has entered a new phase. The central question is no longer whether companies are using AI. That threshold has already been crossed, with AI adoption approaching near-universal levels among many businesses. The real questions now are how deeply companies are using AI, how they are integrating it into operations, and how much AI spending they are willing to absorb.

A June 2026 update to the Ramp AI Index from Ramp Economics Lab offers a data-driven view of this shift. Ramp analyzed aggregated and anonymized corporate card and bill payment data from more than 70,000 U.S. businesses using its platform to track enterprise AI spending trends. The key focus of the latest update was not simple adoption, but adoption intensity. In other words, Ramp moved beyond whether a company subscribes to an AI service and examined how much firms are spending per employee, how spending is divided among AI subscriptions, coding agents, tokens and API usage, and how patterns differ across industries, regions and company sizes.

This shift shows that the AI market is moving beyond its early diffusion stage. In 2023 and 2024, attention focused on whether companies were adopting generative AI tools such as ChatGPT, Claude and Gemini. In 2025, practical use cases expanded rapidly across file summarization, document drafting, customer support and coding assistance. By 2026, the question has become more specific: what separates companies that use AI as a peripheral productivity tool from those that treat it as a core operating system?

Ramp used the phrase “AI-pilled companies” to describe the latter group. The term refers to companies deeply immersed in AI — specifically, the top 1% of firms by AI spending per employee. These companies are not merely handing employees chatbot accounts. They are combining multiple AI vendors, frontier models, coding agents, APIs and AI-native SaaS products to redesign broad parts of their work systems.

The most striking figure is cost. According to Ramp, the top 1% of AI-spending companies are spending $7,449 per employee per month on AI. Companies in the top 10% are spending $611 per employee per month. By contrast, the median company spends just $11.38 per employee per month. That median figure is roughly in the range of a single enterprise seat for a mainstream AI chatbot.

The gap shows that AI adoption is no longer a binary question of whether a company has AI or not. It is now a question of how deeply AI has entered the organization. For the median company, AI remains largely a personal productivity tool. It helps employees polish emails, summarize reports and organize meeting notes. For the top 1%, AI is becoming operational infrastructure that can reshape cost structures, workflows and workforce deployment.

Still, even the most aggressive AI spenders have not yet reached the point where AI spending fully substitutes for human labor costs. Ramp noted that even the top 1% of companies spend less per employee on AI than half the monthly cost of a typical software engineer. Some voices in the technology industry have argued that companies should be willing to spend as much on AI as they would on an engineer’s salary. But actual payment data suggests that this level of spending has not yet become common.

The direction of travel, however, is clear. AI spending is rising. Ramp found that AI spending per employee among the top 1% of companies rose 14.1% from the previous month. Even as cost pressure grows, AI budgets are not shrinking. Companies are also looking for cheaper AI models, but this appears less like an attempt to reduce AI usage and more like an effort to manage cost efficiency as overall AI consumption grows.

This reveals an important feature of the AI market. Companies are not seeking cheaper models because they want to use less AI. They are seeking cheaper models because they want to use more AI. As AI usage expands, token costs, API calls, coding agent fees and workflow automation tools accumulate. Enterprises cannot rely only on the most expensive frontier models for every task. They must combine premium models, lower-cost models, open-source options and specialized solutions according to workload.

This is why companies with advanced AI adoption tend to show weaker dependence on a single vendor. Ramp found that the heaviest AI users often use multiple AI vendors at the same time. They may combine frontier model providers such as OpenAI and Anthropic with platforms that provide access to open-source models, voice agents, industry-specific AI SaaS and AI infrastructure providers.

This suggests that the enterprise AI market may not converge into a single winner-takes-all platform. Instead, it is likely to evolve into a use-case-specific combination market. Companies may use general-purpose chatbots for writing, coding agents for software development, voice agents for customer service and API-based models for internal data analysis. The more deeply companies use AI, the more likely they are to select different models and tools for different workflows rather than standardizing on one brand.

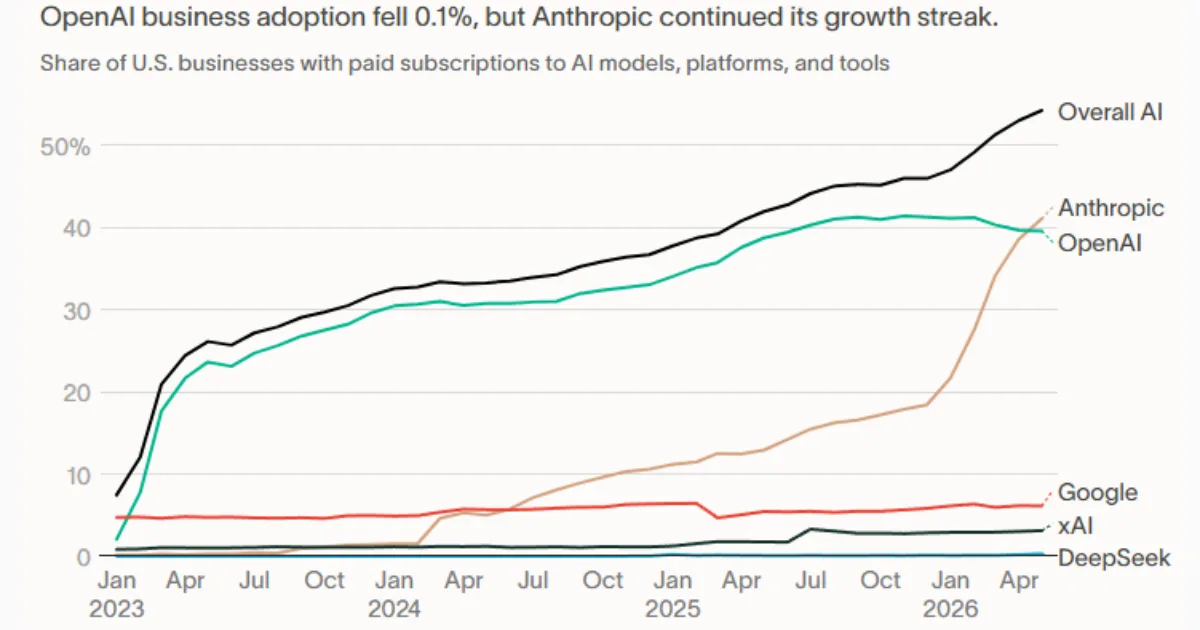

The vendor landscape is also changing. According to Ramp’s June 2026 data, Anthropic reached a 41.0% corporate adoption rate, moving ahead of OpenAI, which stood at 39.5%. The gap between the two companies was 1.5 percentage points. Ramp also said it had updated its methodology to better capture enterprise spending on OpenAI and Anthropic.

The figures suggest that OpenAI remains a powerful player, but Anthropic’s presence in the enterprise market has grown rapidly. In enterprise AI adoption, factors such as security, reliability, long-context capabilities, workflow integration and developer ecosystem carry significant weight. As Anthropic expands its corporate customer base through Claude, OpenAI faces the continuing challenge of defending and expanding its enterprise position.

Yet the essence of the Ramp AI Index is not the ranking of individual vendors. It is the changing structure of enterprise AI spending. Companies no longer view AI simply as another software subscription. AI is becoming an investment category tied to workforce productivity, development speed, customer support, sales automation, data processing and operational optimization. That is why AI spending per employee matters. It acts as a proxy for how deeply AI has entered the way an organization works.

The distance between the median company’s $11.38 per employee per month and the top 1% company’s $7,449 per employee per month represents more than a budget gap. The former reflects the stage in which AI is consumed as a personal productivity service. The latter reflects the stage in which AI becomes a foundation for work systems, product development, customer experience and internal automation. Over time, this gap could become a gap in productivity, workforce structure and speed of market response.

The surge in AI spending also carries important implications for the labor market. If companies are willing to spend hundreds or even thousands of dollars per employee each month on AI, it suggests that AI is moving beyond assistance and beginning to absorb parts of job functions. In software development, customer support, document processing, data analysis, marketing operations and sales support, AI tools are already replacing portions of human time and reducing workflow steps.

That does not mean every company will soon look like the top 1%. AI spending brings clear burdens. As companies adopt more AI tools, they also face growing challenges in cost management, security controls, data governance, model selection, output validation and employee training. More AI usage does not automatically translate into higher productivity. Poorly designed AI adoption can lead to tool sprawl, redundant subscriptions, quality problems and unclear accountability.

For that reason, the next phase of competition will likely separate companies that use a lot of AI from companies that use AI well. High spending among the top 1% may indicate leading-edge experimentation, but it may also include the cost of trial and error. What matters is not the spending level itself, but whether that spending translates into revenue growth, lower costs, shorter work hours or better product quality.

The broader change shown by the Ramp AI Index is that the era of measuring AI adoption by adoption rate alone is fading. Enterprise AI can no longer be understood simply through penetration statistics. In a world where nearly every company uses AI in some form, the decisive issue is who uses it more, who uses it more deeply and who uses it more strategically. A gap is opening between companies that consume AI as a subscription service and companies that embed AI into the operating system of the organization.

That gap could become a new dividing line in corporate competitiveness. Companies that use AI effectively may be able to build products faster with fewer people, respond more quickly to customer inquiries and automate internal decision-making. Companies that use AI only as a surface-level assistant may appear to have adopted AI, but still fall behind in real productivity gains.

Ultimately, the enterprise AI race in 2026 has moved beyond the question of whether AI has been adopted. The more important question is how much AI is changing a company’s cost structure and workflow architecture. Ramp’s data shows that the answer varies dramatically from company to company. For some firms, AI is an $11-a-month subscription per employee. For others, it is core operating infrastructure worth $7,449 per employee per month.

Now that AI has become a necessary business tool, the real competition is only beginning. The decisive gap will not be simple adoption, but intensity of use. It will not be the gap between companies that subscribe and those that do not, but the gap between companies that merely add AI tools and those that redesign themselves around AI. Ramp AI Index’s June update shows that this turning point is already visible in market data.