Layoffs Are a Signal of ''Structural Transformation,'' Not ''Crisis''

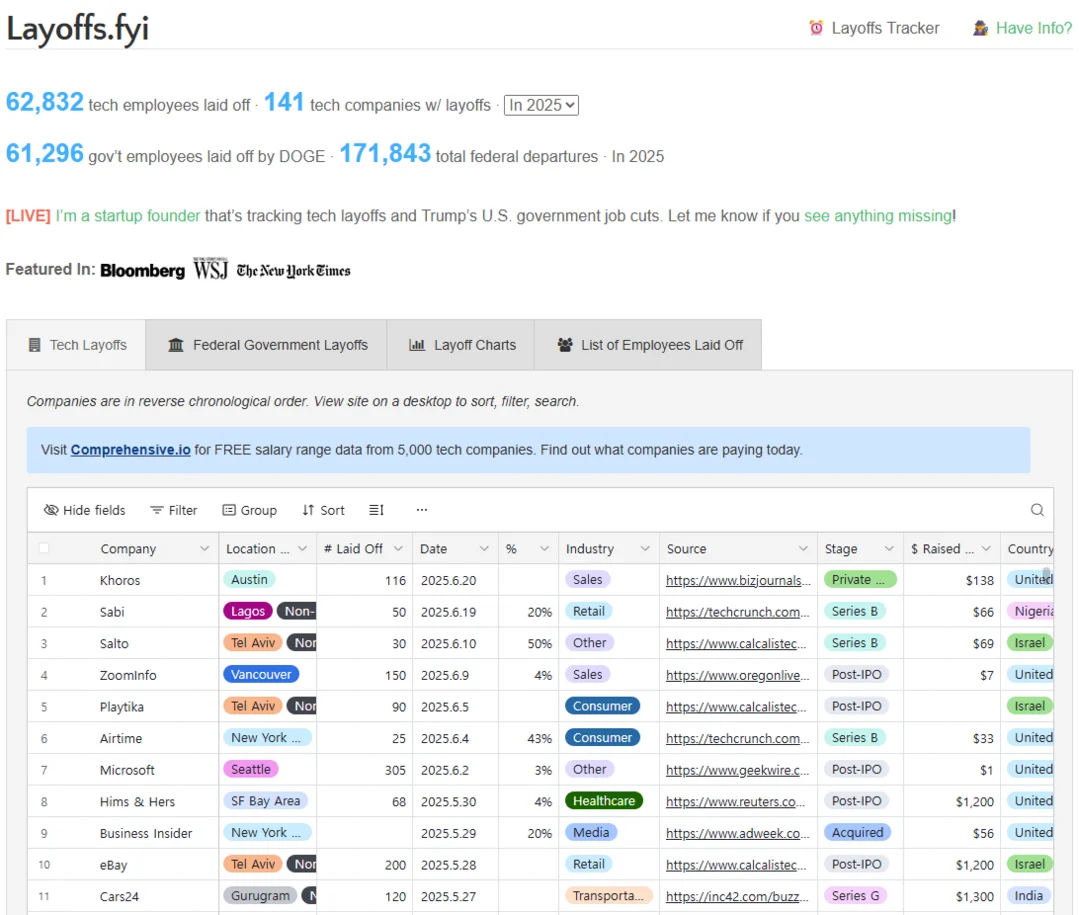

2024-2025 has seen unprecedented structural adjustment in global tech: Amazon, Microsoft, Intel, Meta executing layoffs of thousands — including skilled developers, back-office, HR, and middle managers — with AI-based organizational restructuring and work automation at the center. 2025 H1 tech industry layoffs exceeded 100,000; Layoffs.fyi reports an average of 24,000 layoffs per month since January 2025, exceeding the cumulative layoffs of the 2022-2023 pandemic transition period in a shorter timeframe. The pandemic era "over-expansion": 2020-2021 explosive growth in gaming, cloud, e-commerce, streaming, remote work; global game market revenue grew from $159.3B (2020) to $180.3B (2021, +13%+); US game industry employment grew from ~143,000 (2019) to 428,646 (2021, ~3x in 2 years); Amazon alone hired 500,000+ during the pandemic. Post-pandemic correction: as pandemic-driven demand ended, "growth for growth's sake" hiring proved unsustainable. The structural transition now underway: AI is not merely increasing productivity but fundamentally redesigning workforce structures — eliminating roles that previously required human judgment (QA, content moderation, customer support, data analysis), while creating fewer but higher-skilled AI-adjacent roles. The decoupling: companies achieving record financial performance while simultaneously reducing headcount signals a permanent change in the employment density of the tech industry, not a temporary cyclical adjustment. Policy implications: traditional approaches to tech sector employment (education for tech skills, support for tech worker job transitions) may be insufficient as AI reduces the total number of human positions even in growing companies.