Domestic game companies are estimated to pay around 2 trillion won annually in fees to the Google and Apple app markets. Looking at Netmarble alone, its commission fees in 2025 amounted to 938.7 billion won, accounting for 33% of its revenue. These figures are not simply costs. As the annual revenue of major mobile games grows into the hundreds of billions of won, these fees become a structural burden that directly affects operating profit.

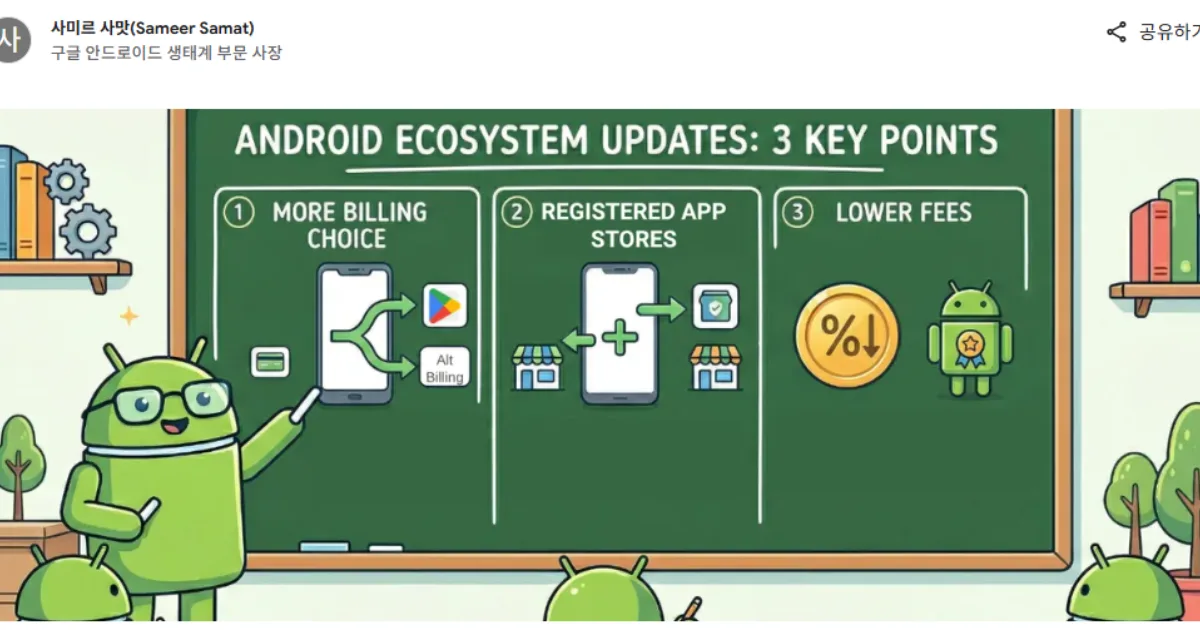

Google recently lowered its in-app payment commission from a previous maximum of 30% to a level centered around 20%, while also expanding the scope of permitted external payments. However, domestic game companies are not simply waiting for this change. They are already expanding PC payments, web shops, and proprietary launchers. In May, industry voices were also raised in Pangyo calling for improvements to the in-app payment fee structures of Google and Apple. Two movements are taking place at the same time: demanding institutional change, while also directly restructuring the payment system without waiting.

Three Responses from the 3N Companies — Netmarble: A Mobile-Centered Model That Proves Fee Reduction Through Numbers

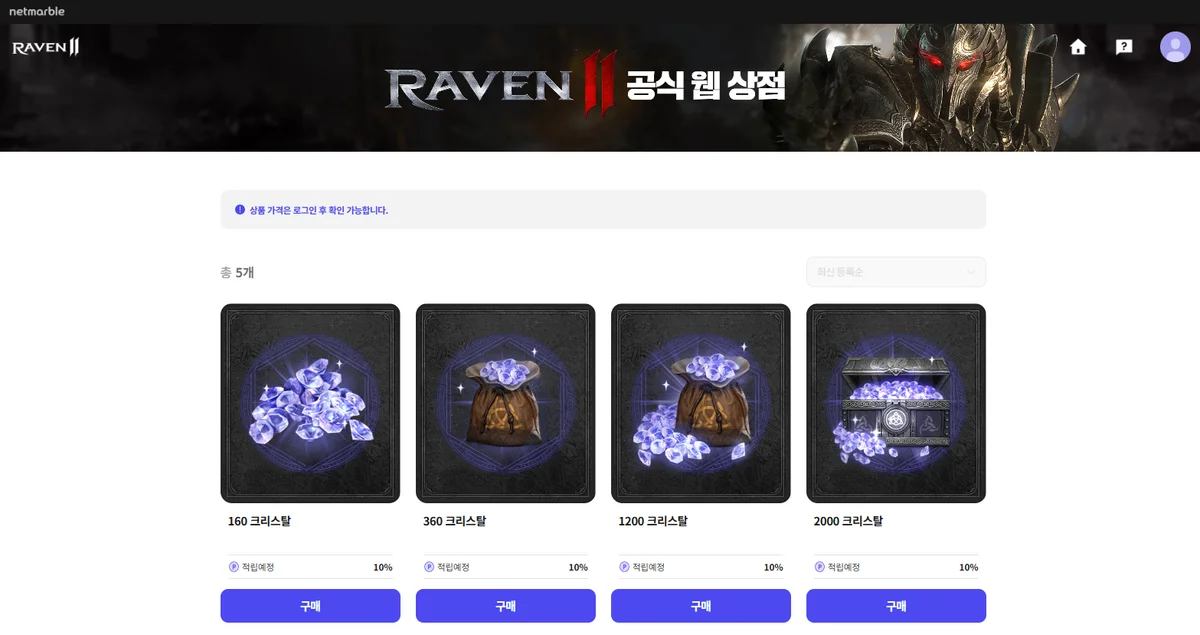

Netmarble began introducing its own payment options alongside major new titles in 2024. For Arthdal Chronicles, it introduced PC payments, a web shop, and a point system together. It also opened web shops for Raven 2 and Solo Leveling: ARISE.

The effect appeared in the numbers. In the first quarter of 2026, Netmarble’s commission fees totaled 200.9 billion won, down 8.3% from the same period the previous year. During the same period, revenue increased year on year to 651.7 billion won, yet commission fees decreased. In other words, it was not simply that revenue had increased. Rather, part of the route through which revenue was generated had changed, altering the company’s cost structure. In its conference call, Netmarble explained that the rising share of PC payments had helped ease the burden of commission fees. Its commission fee ratio also fell from 39% in 2024 to 33.1% in 2025, and is expected to decline further to 29.2% in 2026.

However, the limitations are clear. Netmarble has moved some payment channels outside the app markets, but the inflow route for new users still depends heavily on those app markets. Users discover, install, and update games through app markets. Payments can be redirected, but it is difficult to completely change the first point of contact. Netmarble itself has also stated that it will not apply its own payment system uniformly to every game. This is because the conversion rate to external payments may differ depending on genre and user tendencies. Netmarble is reducing fees, but it has not fully reclaimed the entrance to distribution.

Three Responses from the 3N Companies — NCSoft: A Platform-Internalization Model Centered on PURPLE

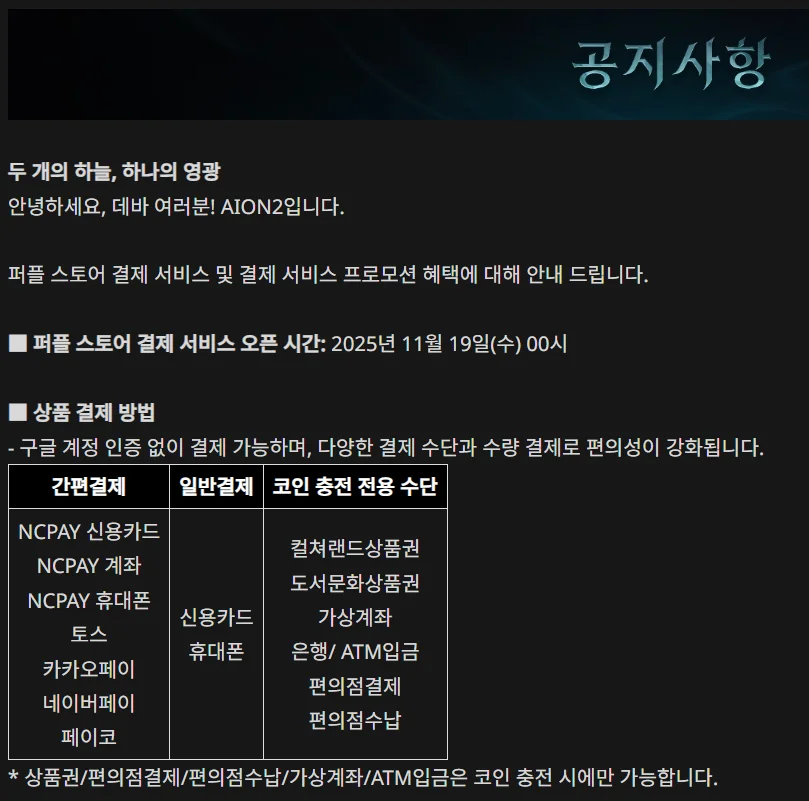

NCSoft’s response has a different character. With the launch of AION 2 in November 2025, the company opened the PURPLE launcher and PURPLE Store payment service together. This was not simply the addition of one more payment channel. It was an attempt to bind game execution, accounts, community, and payments within a single environment called PURPLE. For NCSoft, proprietary payment is not a matter of adding one web shop. It is closer to reconstructing the default route through which users access its games.

The effects are also beginning to appear. As Lineage M users moved away from Google Play and the App Store to PURPLE in order to receive PURPLE payment benefits, analysts have noted that it has become harder to judge the game’s performance solely by app market revenue rankings. The fact that Lineage M, which had maintained a top position in app market revenue rankings for nearly eight years, dropped in the rankings after the shift to PURPLE payments is also interpreted in connection with this change. This does not necessarily mean that revenue disappeared. Rather, it means that the place where revenue is counted has changed.

However, NCSoft still has tasks to solve. A decline in app market rankings may show the movement of existing paying users, but that is a different issue from attracting new users. It remains to be seen whether PURPLE can move beyond changing the payment route of existing users and become a platform capable of drawing in new users on its own. Another challenge is whether a separate launcher and external payment can become a natural route for mobile users. Ultimately, the success of PURPLE will depend not only on payment benefits, but on how smoothly the entire user experience is designed, including game execution, community, and account management.

Three Responses from the 3N Companies — Nexon: A Model That Connects Existing PC Payment Infrastructure to Mobile

Nexon’s approach is quiet, but it has the longest history. Its proprietary payment infrastructure, represented by Nexon ID and Nexon Cash, is an asset that has continued for decades since the era of PC online games. Nexon is less a company urgently building a new platform than one extending its existing account and payment structure into mobile games.

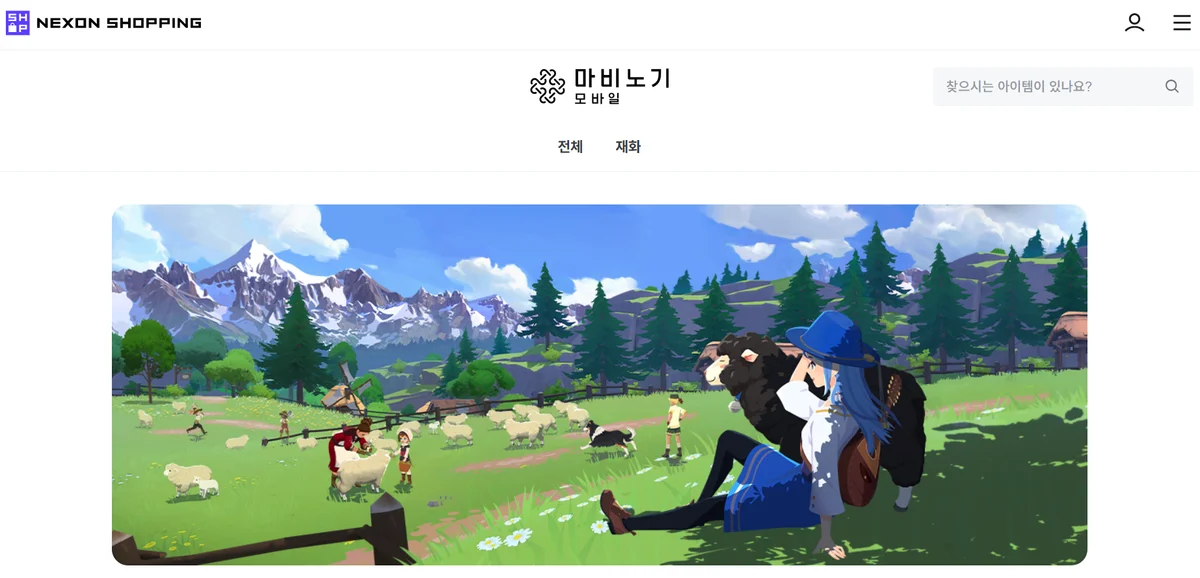

Nexon Shopping is added to this structure. Nexon Shopping is a proprietary payment channel that allows users to purchase items through mobile and PC web pages without directly logging into the game. In the case of Mabinogi Mobile, a store opened within Nexon Shopping in November 2025. Users can purchase products on the web page and receive them through the in-game paid product mailbox. According to the official guide, Nexon Shopping supports the same payment methods as the PC version, and Nexon Cash payments are also available.

Mabinogi Mobile clearly illustrates this structure. In the PC version, users can purchase paid products with Nexon Cash through the Nexon website and the in-game cash shop, and the purchased products can also be checked in the mobile version. Through Nexon Shopping, users can purchase M Cash without logging into the game. In other words, although it is a mobile game, payment is not tied only to the app market. Direct PC payment, Nexon Cash, and Nexon Shopping work together.

This approach differs from those of the other 3N companies. While Netmarble focuses on reducing the fee burden within a mobile-centered business structure, and NCSoft attempts to grow its own platform through PURPLE, Nexon connects its existing PC payment ecosystem to mobile. Nexon Cash, Nexon ID, and Nexon Shopping are not merely payment methods. They are devices that keep users within Nexon’s own account system. For that reason, Nexon’s proprietary payment strategy is less a newly started experiment and more an extension of the long-standing operating model of PC online games.

As a result, Nexon is regarded as having maintained a relatively low commission fee structure. Its long-standing foundation in direct PC payments has become a strength in its cost structure. However, as payment routes increase, the challenge also grows: payment, receipt, refund, and customer support must continue seamlessly no matter which device the user accesses the game from.

Ultimately, Nexon’s strength lies in the long accumulation of payment infrastructure. But for that accumulation to function as a strength in the mobile environment as well, simply increasing payment routes is not enough. The existing PC payment structure must be translated again to fit the mobile user experience.

The Trend Spreads Beyond the 3N Companies

This trend is not limited to the 3N companies. Proprietary payments and web shops are already spreading across mid-sized and large game companies. The key is not only avoiding app market fees. Each company is gradually pulling payment routes into its own operating system in ways that fit its service structure.

Com2uS is expanding Hive-based web shops and third-party payments, using web shops as a practical means of improving profitability. In its first-quarter 2026 conference call, the company explained that although the figure differs by game, the share of payments through web shops ranges from as low as 10% to the mid-20% range. Web shops are no longer simply event pages. They are becoming operational tools that reduce the burden of app market fees.

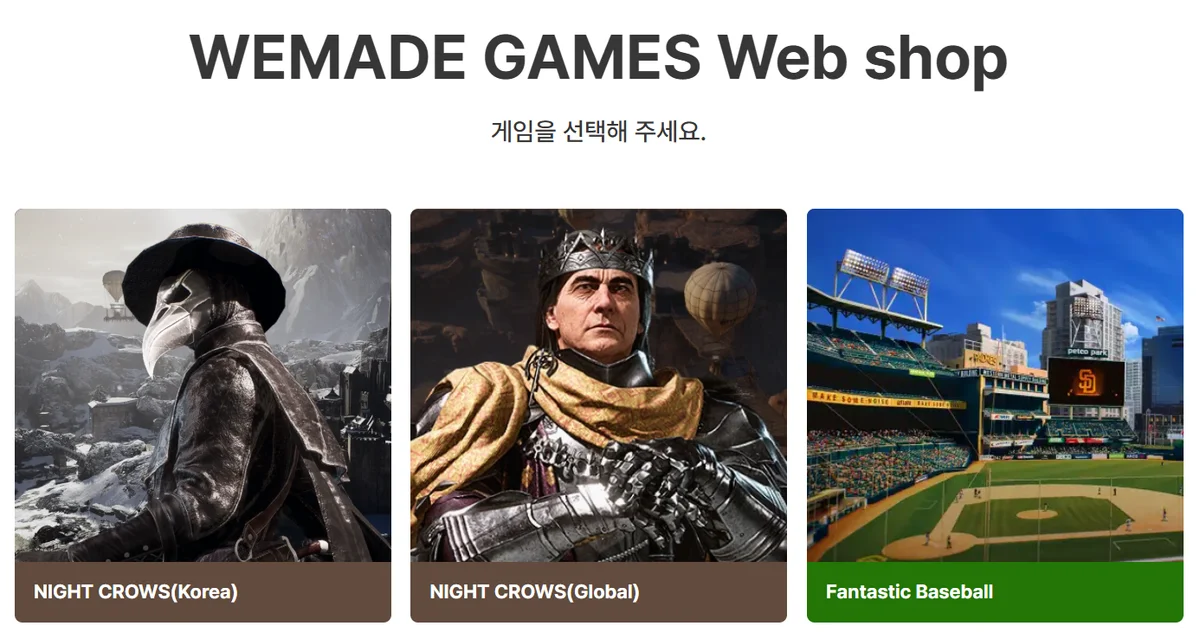

Wemade operates a web shop for Night Crows, combining its cross-platform structure with proprietary payments. The official web shop supports credit card and bank transfer payments, while also offering web shop-exclusive products and benefits. For games used across both PC and mobile, web shops can connect relatively naturally as payment routes outside the app market.

Kakao Games also operates a web shop for ArcheAge War. Rather than saying, as in older phrasing, that it is “under review,” it is more accurate to treat it as a case in which a web shop already exists. This shows that proprietary payment is not an experimental choice by only a few companies, but is gradually becoming a basic option in the operation of major MMORPGs.

Pearl Abyss is a slightly different case. Black Desert has long operated an Acoin charging system and an official website payment structure. Rather than being a case in which a new web shop was created to bypass mobile app markets, Pearl Abyss is closer to a company that originally had a strong foundation in direct PC service and proprietary payments. In the current trend, therefore, Pearl Abyss is better understood not as an “experiment in escaping app markets,” but as a case in which an existing direct-service model is receiving renewed attention.

Ultimately, proprietary payment is no longer an exceptional experiment by a few major companies. It is becoming a realistic industry-wide choice for reducing dependence on app markets and bringing payment data and product design authority into each company’s own operating system.

Why This Is a Question of Platform Control

Why does reclaiming the payment route go beyond simple cost reduction? It can be summarized in three points.

First, when a company brings the payment route under its control, it gains product design authority. Within app markets, companies must operate within the framework of platform policies. With proprietary payments, game companies can directly design points, discounts, packages, memberships, partnership benefits, and web shop-exclusive products. They can create structures that attract users and keep them engaged.

Second, payment data is live-service operation data. What products were purchased, when payments were made, which events users responded to, and how PC and mobile payment patterns differ are all operational signals. The payment flows of high-spending users and returning users also reveal patterns. Proprietary payment is both a payment method and a device for collecting operational data. When payment takes place within an app market, that data belongs to the platform.

Third, the payment contact point is the final stage of the user relationship. Game companies create content, operate events, and manage communities. But if payment ends inside the app market, the platform takes the most important moment of contact with the user. Proprietary payment is an attempt to bring that final stage back to the game company.

Of course, a complete escape from app markets is realistically difficult. App markets remain the core route for downloads and new user acquisition, and mobile users are accustomed to in-app payments. Proprietary payment infrastructure is a feasible option for large companies, but for smaller companies, the operating cost itself is a burden. Reclaiming payment means reducing fees, but it also means reclaiming the authority to design revenue, read data, and directly manage user relationships.

All Platforms Are Fighting for the Final Point of Contact

The issue of game payments is not an isolated incident.

The AI search update unveiled at Google I/O in May 2026 clearly shows this trend. Search is no longer merely a window that lists links. Google described its AI search box as its “biggest upgrade in 25 years,” presenting a direction in which AI responses, recommendations, shopping, and agent functions are combined within search. This is a movement in which the search platform attempts to reclaim the final point of contact where content is discovered, compared, and connected to purchase.

Android XR smart glasses are part of the same context. At I/O 2026, Google introduced Gemini-based intelligent glasses and presented two directions: audio glasses that provide guidance through the ears, and display glasses that show information within the user’s field of vision. If the user contact point after smartphones moves from the screen in the hand to sight and voice, platform competition will once again take place directly in front of the user’s eyes.

The restructuring of the streaming industry is similar. Paramount Skydance agreed in February 2026 to acquire Warner Bros. Discovery for around 110 billion dollars, with the transaction aiming to close in the third quarter of 2026 after regulatory review. This trend shows that simply owning a large amount of content is not enough. What matters is where the content is shown, who recommends it, and who controls the subscription and advertising relationship.

AI, XR, streaming, consoles, and mobile game payments may appear to be separate incidents. But they all converge on the same question: who will own the final point of contact with the user?

The expansion of proprietary payments by domestic game companies is one scene in this broader competition. It is a movement to reduce fees, but at a deeper level, it is an attempt to bring the moment when users decide to pay back toward the game company.

Reclaimed Payments, Remaining Platforms

Expanding proprietary payments, opening web shops, and building proprietary launchers are now only the beginning.

The gap between large companies and smaller companies may widen further. Web shops, launchers, and point systems all require infrastructure and operating costs. Only a limited number of companies can turn proprietary payment into a practical tool. The payment monopoly of app markets may weaken, but their influence as platforms for distribution, exposure, trust, and authentication will remain. Users discover and install games through app markets. That first point of contact does not change. Ultimately, we are entering an era in which the competitiveness of game companies is no longer determined only by their ability to make good games. Proprietary payments, data analysis, account platforms, and cross-platform experience design all become important together.

What domestic game companies are trying to reclaim is not a few percentage points of fees.

The real question comes next.

Can game companies, after reclaiming payments, also build their own platforms where users will continue to stay?